According to CBN figures, Nigeria’s 12-month moving average inflation read 18.85% in December 2022 for all items, after a turbulent year with global price pressures. Inflation continues to rise with February 2023 showing a 24.35% year-on-year (YoY) rise in foods and 21.91% over all items(YoY). In the coming months, inflation figures should ‘slow’ down. This is only nominally true because inflation is calculated based on YoY changes. Price rises are very sticky and a lower inflation reading based on already elevated prices results in a smaller percentage rise but a larger total increase.

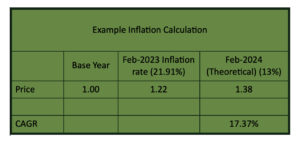

The example above illustrates an example calculation of the effect of inflation on prices. The starting price was 1.00 and ~1.22 after official YoY inflation data from the CBN. If inflation runs at 13% next year in Nigeria prices will have gone from 1.00 to ~1.38 in two years, with a cumulative aggregate growth rate (CAGR) of 17.37%. CAGR represents average yearly growth over the two-year period. The minimum wage in Nigeria has remained at 30,000N since 2019 for contracted employees. Inflation over that same period has eroded more than 50% of purchasing power.

It is difficult to pinpoint the causes of inflation, however, one area for concern regarding Nigeria’s inflation would be its balance of trade. Nigeria’s inflation gauge is heavily weighted with foodstuffs. Food prices are currently Nigeria’s biggest inflation driver.

Nigeria has become the US’ fifth largest importer of wheat, importing 1.29 million metric tons in 2020. Total agricultural imports from the US averaged over the past five years (2016-2021) $537 million. US wheat imports account for only 40% of Nigeria’s total wheat imports, with Russia accounting for a substantial portion of the remaining imports. Nigeria only manages to export $50 million worth of agricultural products. The importation of agricultural products is not a concern by itself. However, compounding issues such as a high growth rate in consumption as preferences change coupled with high population growth may lead to the undermining of Nigeria’s sovereignty. Nigeria is forecasted to import 10 million metric tonnes of wheat annually by 2030.

The balance of trade for Nigeria, calculated as exports minus imports, stood at -$4.85 billion in 2021, an 870% increase from 2020. Nigeria uses its foreign currency reserves such as the US dollar and Euro to pay for these imports on international markets. It receives US dollars and Euros when it exports its goods. However, with such an imbalance of trade, Nigeria is at a net loss of foreign currency reserves. More money is leaving Nigeria to foreign producers than Nigeria is getting in return for its own production. Additionally, a dependence on imports exposes Nigeria’s economy to supply shocks, such as the Russia-Ukraine war which saw the price of wheat increase dramatically on international markets. Price rises in international markets are something Nigeria cannot control. However, dependency on imports such as wheat will have serious consequences for poorer Nigerians who depend on these products. Domestic production would help offset these shocks as price rises would not depend on external shocks and foreign exchange rates. Investment in agricultural infrastructure requires large upfront costs and a long investment horizon, something that must be done and will require a lot of political will.

Similarly, Nigeria’s largest export by revenue is oil. However, the production and development of Nigerian oil stumbled over the past couple of years, steadily reducing the inflow of foreign currency to Nigeria. Oil is the driving force behind Nigeria’s balance of trade, causing it to fluctuate YoY, dependent on oil prices in international markets. Low investment and production of oil hindered Nigeria’s capacity to earn large windfalls on oil prices since the Russia-Ukraine war.

The dependency on wheat as an import and oil as an export has without a doubt exacerbated inflation in Nigeria. The dependency on foreign markets has hamstrung the CBN’s ability to tame inflation. Orthodox monetary policy cannot by itself combat fluctuations in foreign markets. The CBN’s ability to control inflation is sacrosanct to the institution of a central bank. A lack of ability to control price rises reduces Nigeria’s sovereignty and puts its people at the whim of foreign markets. Bolstering domestic food production and consumption will drive domestic investments and in the long-run stability. It is not only economically necessary but a matter of national security.

In the coming months, inflation may be reportedly ‘cooling off’ as policymakers try to find positive spins. Inflation increases may be cooling off in comparison to prior YoY readings, however, price rises are already baked in, resulting in lower nominal readings but large increases in nominal prices.