The Lagos State Government has announced a new, more stringent approach to recovering unpaid taxes, which includes directly accessing defaulters’ bank accounts and compelling payments through third parties such as employers, tenants, debtors, and business associates. This move aims to enhance tax collection efficiency and ensure that outstanding tax liabilities are settled promptly.

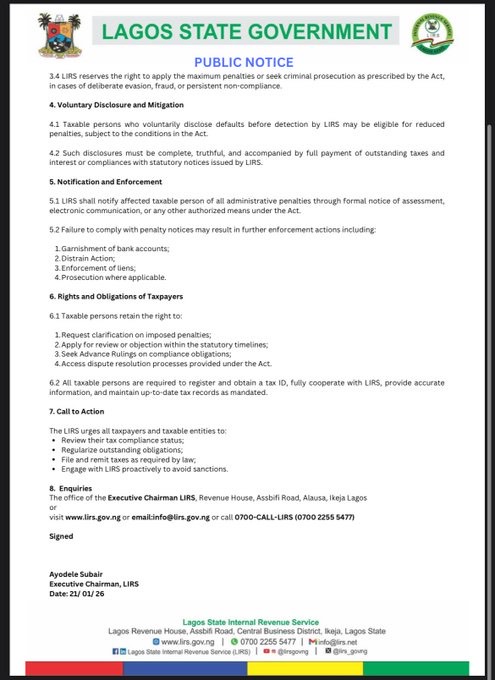

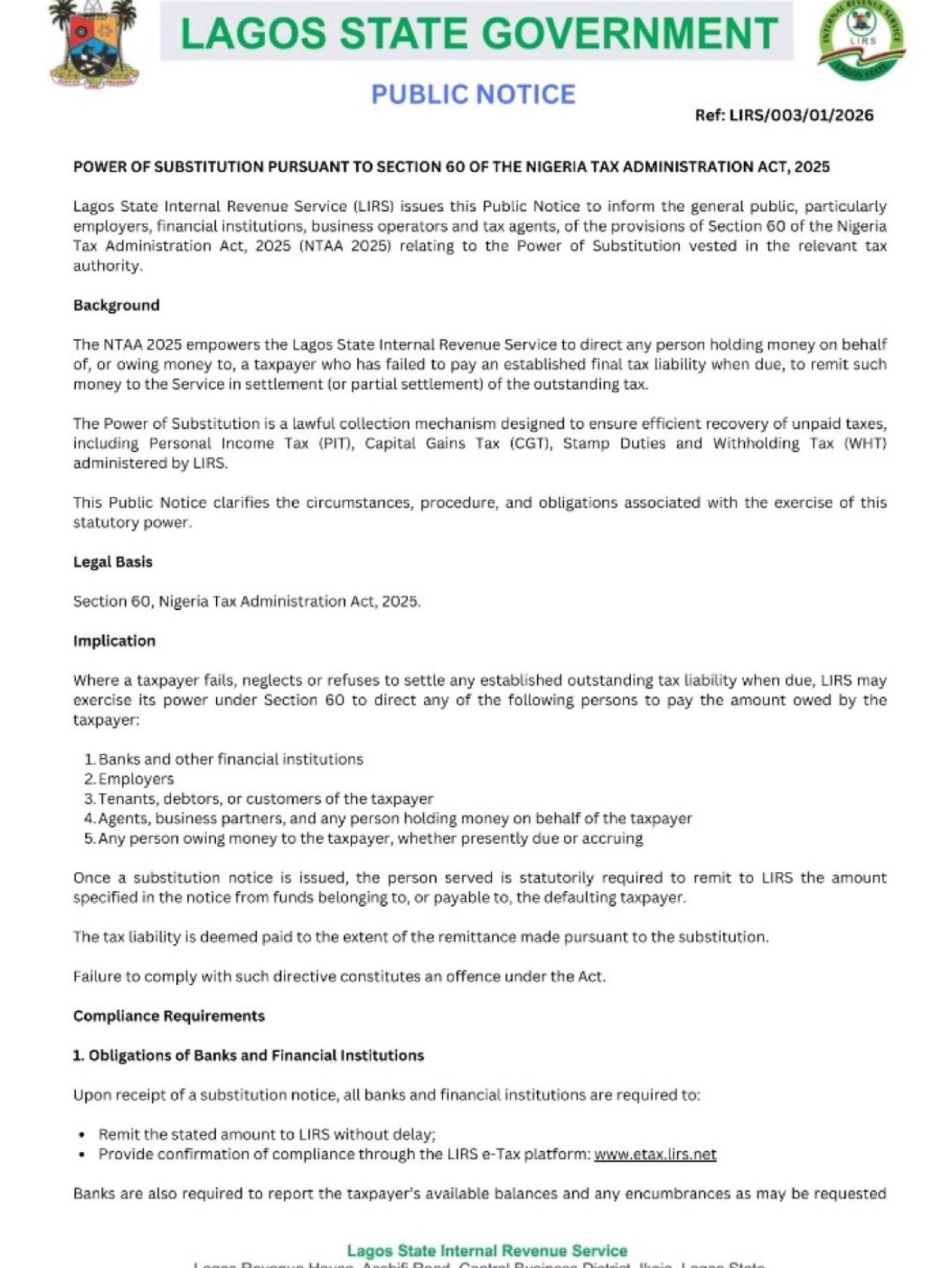

This announcement comes from the Lagos State Internal Revenue Service (LIRS) through a public notice detailing the agency’s newly empowered enforcement measures under the “Power of Substitution,” as outlined in Section 60 of the Nigeria Tax Administration Act, 2025 (NTAA 2025). The notice, signed by the Executive Chairman of LIRS, Ayodele Subair, and dated January 21, 2026, provides clarity on how this authority will be exercised.

LIRS specifically addressed the general public, including employers, financial institutions, business operators, and tax agents, highlighting the provisions of the NTAA 2025 that grant the tax authority the power to direct third parties holding or owing money to taxpayers with unpaid tax liabilities to remit such funds directly to the revenue service. This means that if a taxpayer fails to meet their tax obligations after assessment, LIRS can legally instruct these third parties to pay the outstanding amounts on the taxpayer’s behalf.

This power of substitution is described by LIRS as a legitimate and necessary tool to facilitate the collection of various tax types under its jurisdiction, including Personal Income Tax (PIT), Capital Gains Tax (CGT), Stamp Duties, and Withholding Tax (WHT). The measure is aimed at minimizing tax evasion and ensuring government revenues are protected.

The notice underscores that if a taxpayer neglects or refuses to pay an assessed tax liability, LIRS may invoke Section 60 to compel payment from entities such as banks, employers, tenants, debtors, customers, agents, business partners, or anyone holding money owed to the taxpayer, whether currently due or upcoming. Once a substitution notice is served, the instructed party is legally obligated to remit the specified funds to LIRS without delay.

Importantly, the tax debt is considered settled to the extent that the third party has transferred funds to LIRS in compliance with the substitution directive. Non-compliance with this directive is classified as an offence under the Nigeria Tax Administration Act, exposing the defaulter and any non-compliant third parties to potential penalties.

For banks and other financial institutions, LIRS emphasizes a swift response upon receipt of substitution notices. These institutions must transfer the designated amounts promptly and confirm compliance through LIRS’s electronic tax platform (e-Tax). Additionally, banks are required to disclose the taxpayer’s available account balances and any legal claims or encumbrances, if requested by the revenue service.

The agency warns that deliberate evasion, fraudulent acts, or repeated failures to comply with these enforcement directives will attract severe sanctions. These may include maximum penalties and even criminal prosecution as stipulated by the Act.

Regarding enforcement, LIRS will notify taxpayers of penalties and compliance issues through official notices, electronic communications, or other authorized methods. Failure to adhere to tax obligations may trigger aggressive collection actions such as garnishment of bank accounts, distraint (seizure of property), enforcement of liens, and prosecution where warranted.

Despite the strict enforcement measures, taxpayers retain rights to due process. They can seek clarifications on penalties imposed, request reviews or file objections within the timelines specified by law, and apply for Advance Rulings to clarify their compliance duties. Dispute resolution mechanisms provided under the Act remain accessible for resolving disagreements.

In conclusion, the Lagos State Internal Revenue Service urges all residents and businesses to proactively assess their tax compliance status. The agency calls on taxpayers to regularize any outstanding payments, file all necessary returns, and fulfill their tax responsibilities to avoid punitive actions. Early engagement with LIRS and adherence to tax laws will help taxpayers steer clear of sanctions and contribute to the state’s economic growth.